Renasant has had an impressive run over the past six months as its shares have beaten the S&P 500 by 5.3%. The stock now trades at $38.20, marking a 12.9% gain. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Renasant, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Renasant Not Exciting?

We’re happy investors have made money, but we're cautious about Renasant. Here are three reasons why there are better opportunities than RNST and a stock we'd rather own.

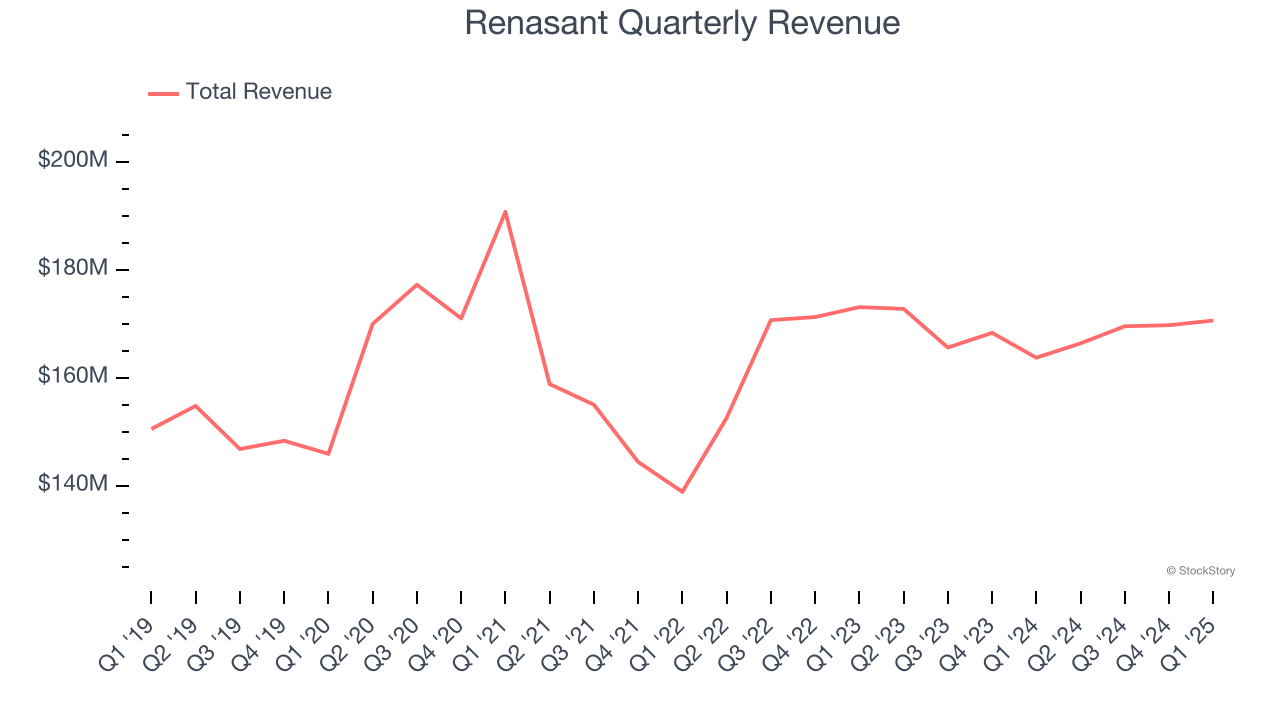

1. Long-Term Revenue Growth Disappoints

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Regrettably, Renasant’s revenue grew at a tepid 2.6% compounded annual growth rate over the last five years. This fell short of our benchmarks.

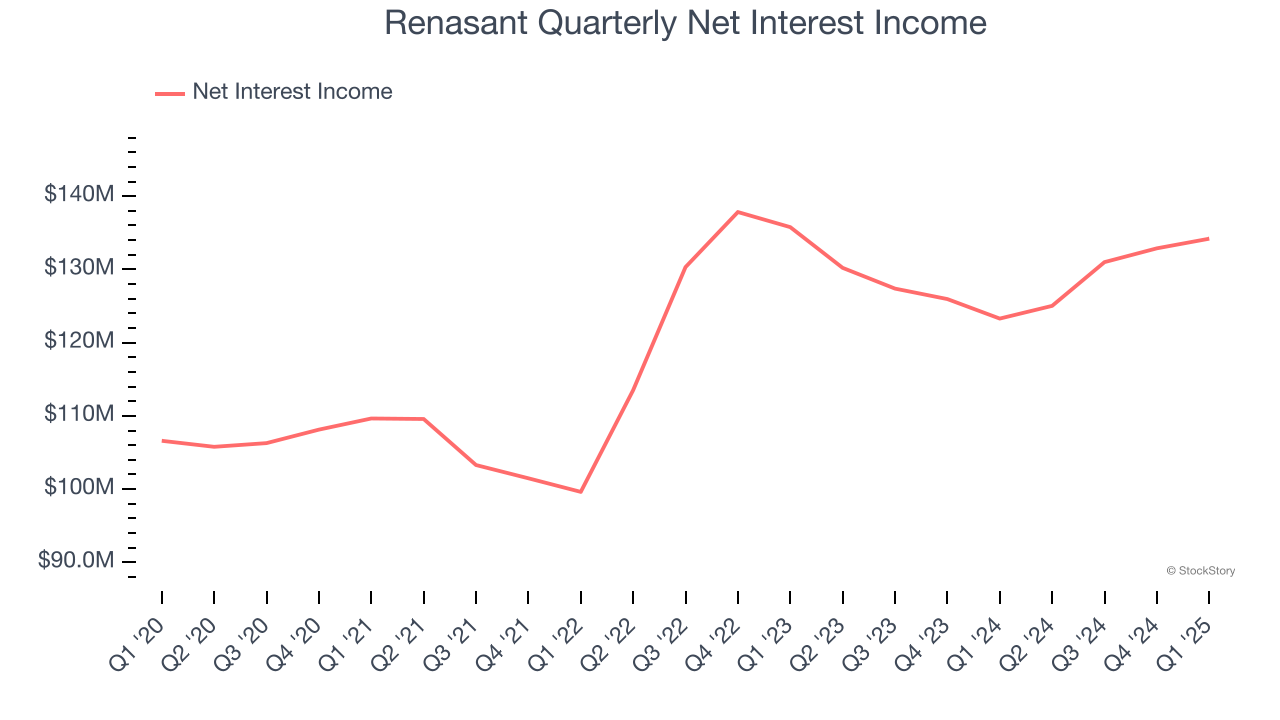

2. Net Interest Income Points to Soft Demand

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

Renasant’s net interest income has grown at a 5% annualized rate over the last four years, worse than the broader bank industry.

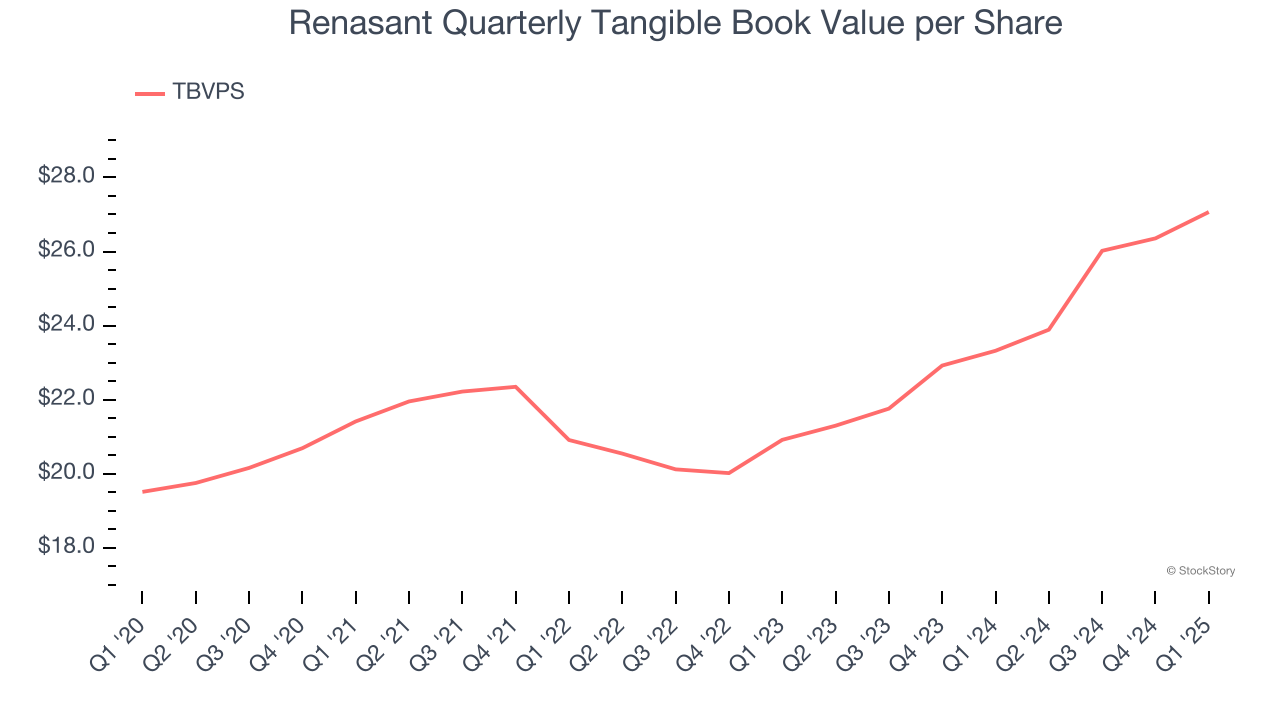

3. TBVPS Projections Show Stormy Skies Ahead

Tangible book value per share (TBVPS) growth comes from a bank’s ability to profitably lend while maintaining prudent risk management and efficient operations.

Over the next 12 months, Consensus estimates call for Renasant’s TBVPS to shrink by 9.9% to $24.40, a sour projection.

Final Judgment

Renasant’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 0.9× forward P/B (or $38.20 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.