BNY Mellon has been on fire lately. In the past six months alone, the company’s stock price has rocketed 45.5%, reaching $106.92 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy BNY Mellon, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Why Is BNY Mellon Not Exciting?

Despite the momentum, we're sitting this one out for now. Here are three reasons there are better opportunities than BK and a stock we'd rather own.

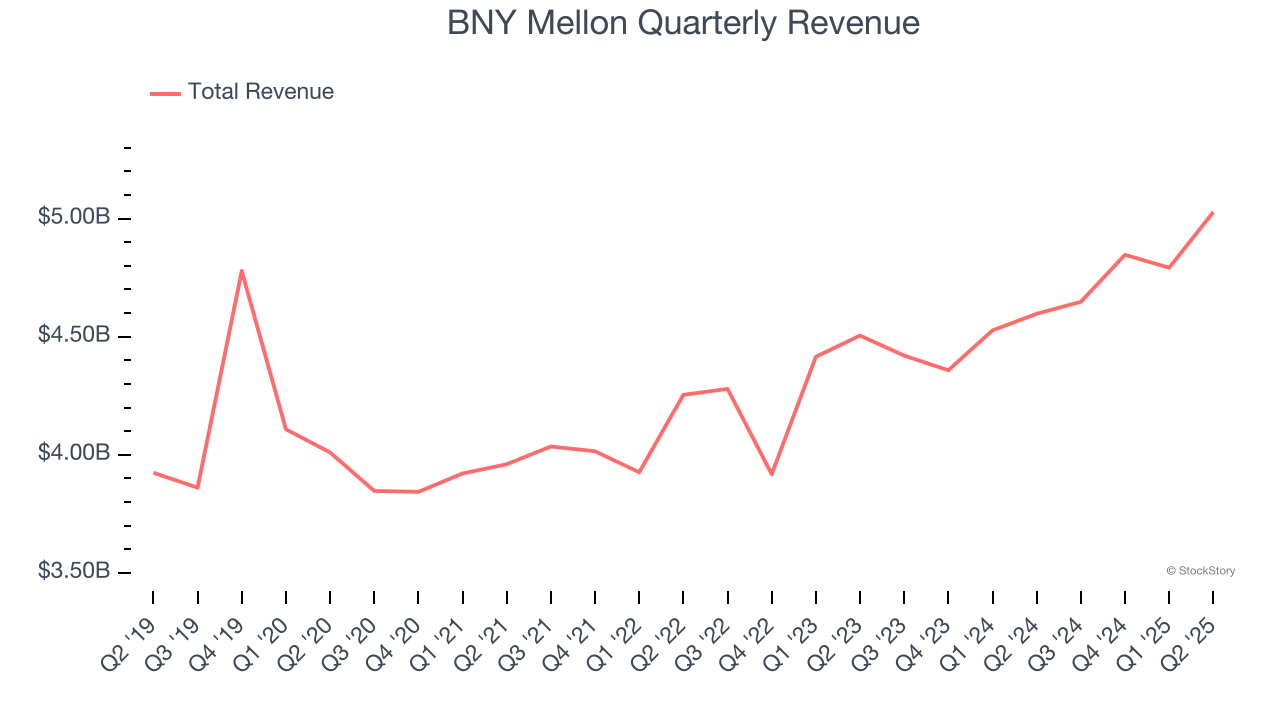

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

Unfortunately, BNY Mellon’s 2.9% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks.

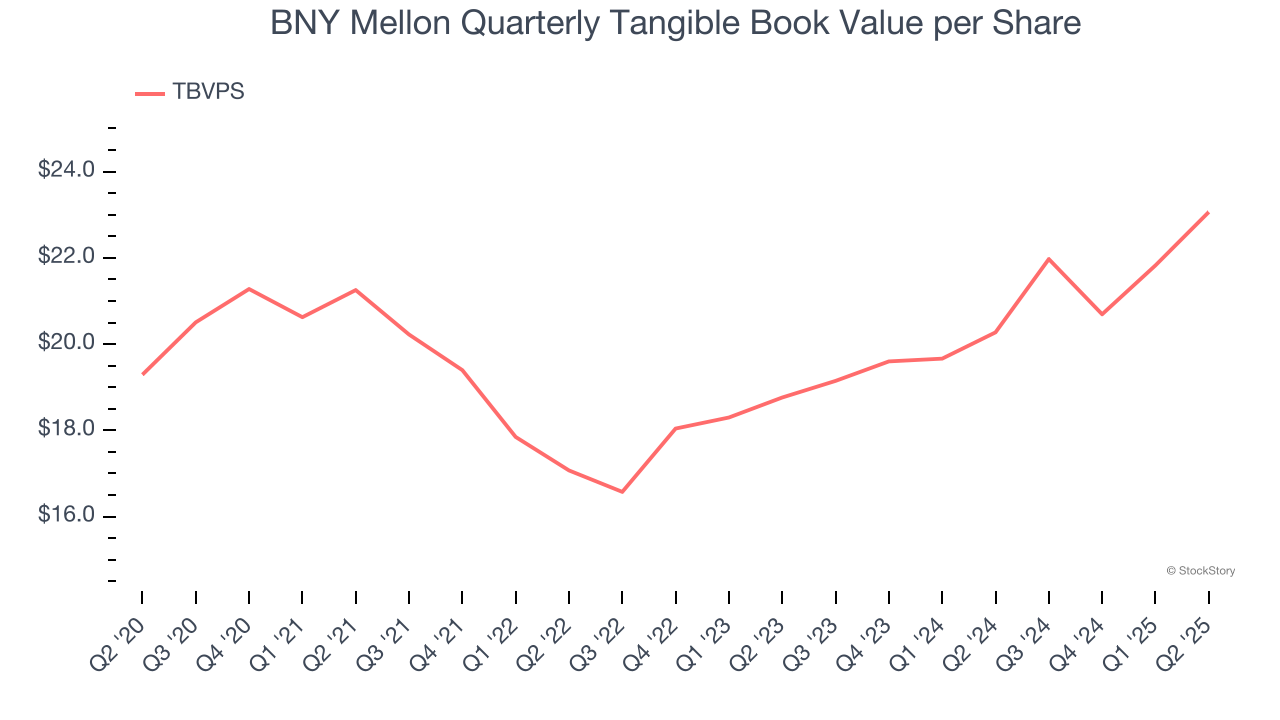

2. Steady Increase in TBVPS Highlights Solid Asset Growth

We consider tangible book value per share (TBVPS) an important metric for financial firms. TBVPS represents the real, liquid net worth per share of a company, excluding intangible assets that have debatable value upon liquidation.

Although BNY Mellon’s TBVPS increased by a meager 3.6% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at a solid 10.9% annual clip over the past two years (from $18.76 to $23.06 per share).

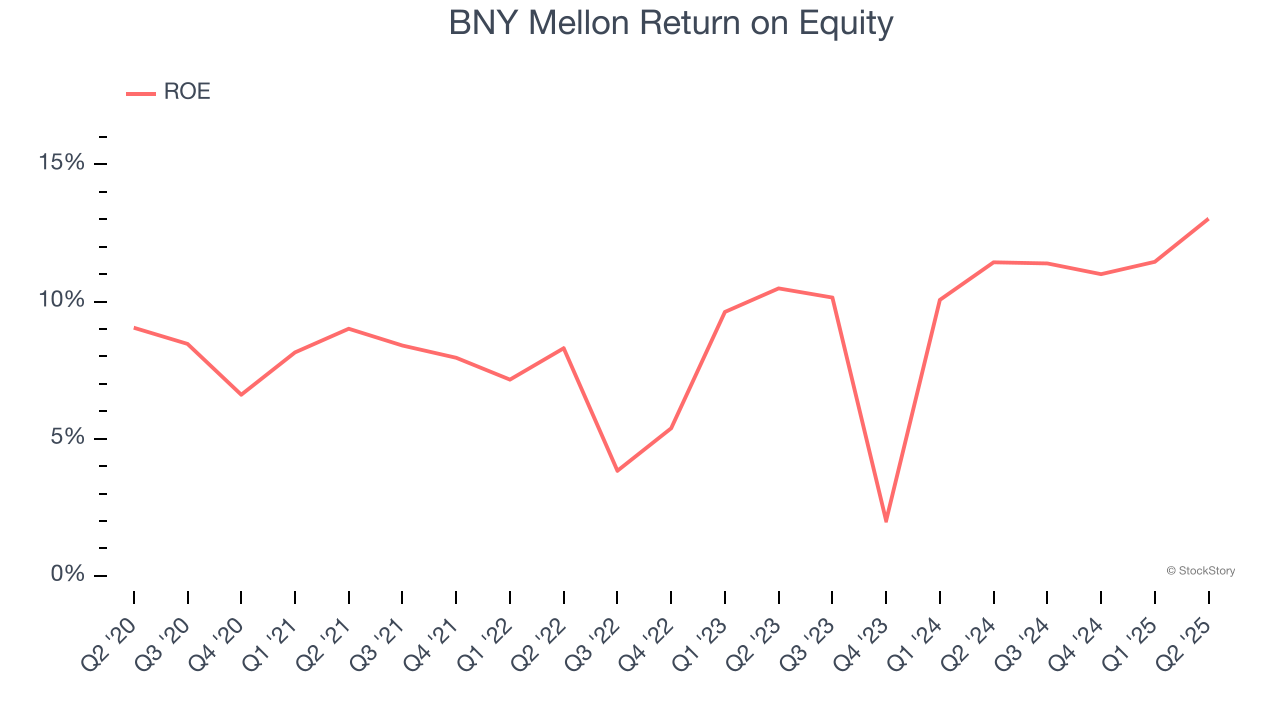

3. Previous Growth Initiatives Haven’t Impressed

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, BNY Mellon has averaged an ROE of 8.7%, uninspiring for a company operating in a sector where the average shakes out around 10%.

Final Judgment

BNY Mellon’s business quality ultimately falls short of our standards. After the recent rally, the stock trades at 14.4× forward P/E (or $106.92 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than BNY Mellon

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.